AI Deep Research 1: Ford-CATL Partnership: FEOC Risk

Strategic Reconfiguration of American Battery Supply Chains: The Ford-CATL Licensing Model under the OBBBA Regulatory Regime

The contemporary transformation of the United States automotive industry is defined by a paradox of technological necessity and geopolitical resistance. At the center of this tension lies the strategic partnership between Ford Motor Company and Contemporary Amperex Technology Co. Limited (CATL), an arrangement that has become the primary case study for how Western industrial giants attempt to domesticate advanced Chinese battery technology while navigating an increasingly hostile regulatory environment. This partnership, centered on the BlueOval Battery Park Michigan project in Marshall, Michigan, was initially conceived as a mechanism to bypass the Foreign Entity of Concern (FEOC) restrictions established by the Inflation Reduction Act (IRA) of 2022. However, the enactment of the One Big Beautiful Bill Act (OBBBA) on July 4, 2025, has introduced a more stringent "Prohibited Foreign Entity" (PFE) framework that fundamentally challenges the long-term viability of this licensing-based strategy.

The Business Architecture of the Ford-CATL Partnership

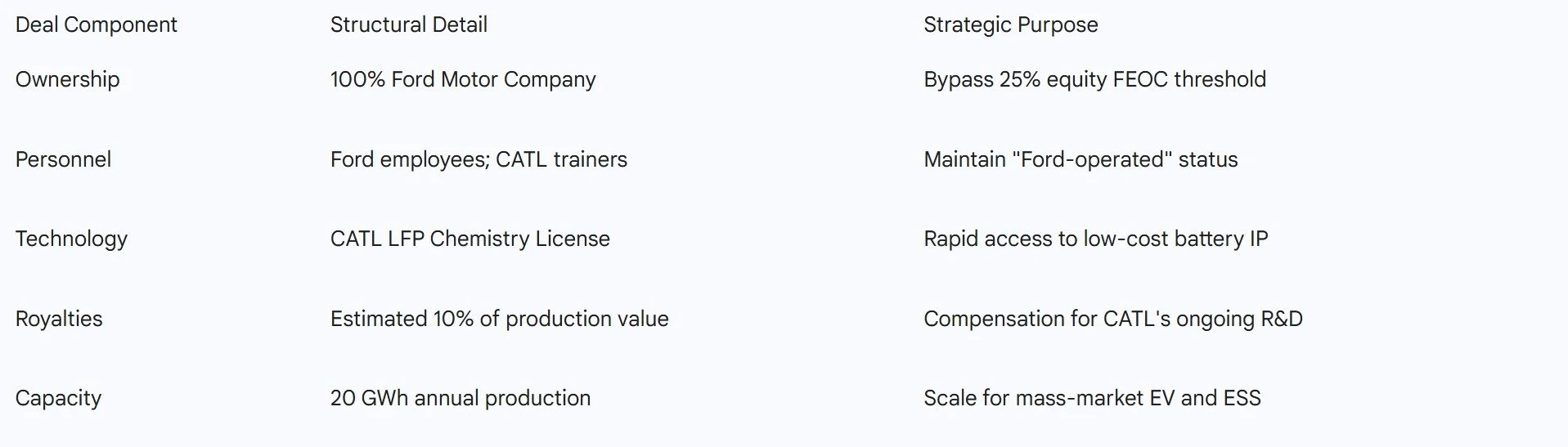

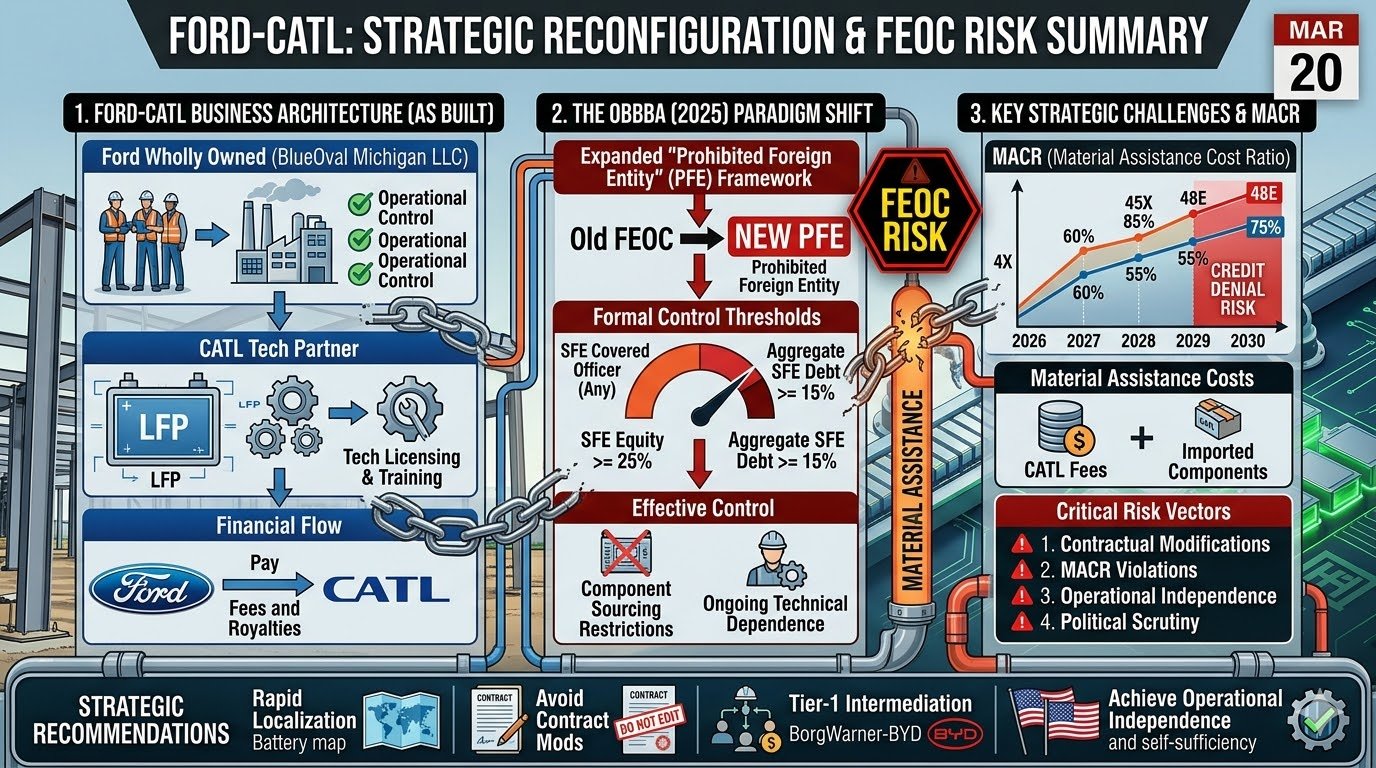

The partnership between Ford and CATL is structured not as a traditional equity joint venture, but as a comprehensive technology licensing and services agreement. This distinction is the cornerstone of Ford’s strategy to maintain eligibility for federal manufacturing subsidies. Under the terms of the deal, Ford established a wholly owned subsidiary, BlueOval Battery Michigan LLC, which maintains 100% ownership of the facility, the land, and the production equipment. Ford serves as the employer of record for the site’s projected workforce, which is expected to reach 1,700 high-paying manufacturing jobs by 2026.

The role of CATL is restricted to that of a technical partner. The Chinese firm provides the intellectual property (IP) for lithium iron phosphate (LFP) battery chemistry, shares its proprietary manufacturing processes, and provides personnel to assist with equipment installation and worker training. In exchange, Ford pays CATL licensing fees and royalties, reportedly structured as approximately 10% of the production value. This model allows Ford to claim that the project is "Ford-owned and Ford-operated," a legal distinction designed to insulate the project from being classified as a foreign-controlled operation.

Rationale for the Licensing Strategy over Equity Joint Ventures

Ford’s decision to avoid an equity-based joint venture was driven by the necessity to comply with the 25% ownership threshold established in early Department of Energy (DOE) guidance regarding FEOC status. By retaining 100% equity, Ford effectively bypassed the "ownership" prong of the FEOC definition. Furthermore, the licensing model addresses the "speed to market" challenge. Ford executives have acknowledged that developing domestic LFP technology independently would have required at least a decade of internal research and development. Given that LFP batteries are significantly more cost-effective than nickel-manganese-cobalt (NMC) variants—due to the absence of expensive materials like cobalt and nickel—they are essential for Ford’s plan to produce affordable electric vehicles, such as its projected $30,000 electric truck.

The business logic extends beyond immediate vehicle production. In late 2025, Ford expanded the scope of the CATL partnership to include stationary energy storage systems (ESS), targeting data centers and grid-scale applications. This pivot reflects an effort to maximize the utilization of the Marshall facility’s 20 GWh capacity as the consumer EV market experiences a period of slower growth.

Regulatory Navigation: Bypassing the FEOC Designation

The initial success of the Ford-CATL deal in avoiding the FEOC label was predicated on a precise interpretation of the Department of Energy’s 2024 final interpretive guidance. This guidance established that an entity is a FEOC if it is "owned by, controlled by, or subject to the jurisdiction or direction of a government of a foreign country that is a covered nation" (China, Russia, Iran, North Korea).

The Three-Pronged FEOC Test

The DOE guidance identified three primary mechanisms for FEOC designation. First, jurisdictional control is established if an entity is incorporated in, headquartered in, or performs its relevant activities in a covered nation. Second, ownership control is triggered if 25% or more of an entity's voting rights, board seats, or equity interests are held—directly or indirectly—by the government of a covered nation or its instrumentalities. Third, effective control can be established through contracts or licenses that grant a foreign entity the right to direct operations or limit the licensee's autonomy.

Ford’s project was designed to fail all three prongs of the FEOC test. The subsidiary is incorporated in Michigan, has 0% Chinese equity, and maintains operational autonomy. Ford’s leadership has repeatedly defended the "Ford-owned and Ford-operated" claim, arguing that the licensing agreement does not provide CATL with the power to "direct" the company’s manufacturing activities or dictate the disposition of the final products. By positioning the agreement as a simple commercial procurement of intellectual property, Ford aimed to place the partnership outside the reach of national security-related investment reviews like those conducted by the Committee on Foreign Investment in the United States (CFIUS).

The Paradigm Shift: The One Big Beautiful Bill Act (OBBBA) of 2025

The legal landscape shifted dramatically on July 4, 2025, with the signing of the OBBBA, a centerpiece of President Trump’s second-term economic agenda. The OBBBA significantly expands the scope of foreign entity restrictions, moving from the IRA’s FEOC framework to a more aggressive "Prohibited Foreign Entity" (PFE) and "Foreign Influenced Entity" (FIE) regime.

New Definitions of Control and Influence

Under the OBBBA, the PFE category includes Specified Foreign Entities (SFEs) and Foreign Influenced Entities (FIEs). An SFE is defined mechanically to include any entity on several national security lists, including Chinese military companies, as well as any entity incorporated in or controlled by a covered nation. An FIE is a domestic entity that falls under the "formal" or "effective" control of an SFE.

Formal control under the OBBBA is triggered by several thresholds that are more expansive than the previous 25% rule:

The authority of an SFE to directly or indirectly appoint a "covered officer" (including CEO, COO, CFO, or board members).

A single SFE owning at least 25% of the entity’s stock.

Multiple SFEs owning 40% or more of the entity in the aggregate.

At least 15% of the entity's debt being held by SFEs (measured at the time of original issuance).

This new framework poses a specific threat to the Ford-CATL model through the "effective control" provision. The OBBBA defines effective control to include any licensing agreement where a PFE counterparty retains the right to specify sources of components, restrict access to site data, or if the arrangement does not provide the licensee with all necessary technical know-how to operate the facility without the PFE's ongoing involvement.

Risks of FEOC/PFE Labeling for the Ford Partnership

The risk of the Ford-CATL partnership being labeled as an FIE or a prohibited arrangement has increased due to the political and legislative scrutiny surrounding the Marshall plant. The primary risk vectors involve the "Specified Foreign Entity" status of CATL and the "Material Assistance" restrictions applied to the Section 45X and 48E tax credits.

Military Company Designations and Political Pressure

The House Select Committee on the CCP has been vocal in its opposition to the Ford-CATL deal, specifically identifying CATL as a "Pentagon-designated Chinese military company" and a "Department of War-designated Chinese military company". Under the OBBBA, these designations are sufficient to classify CATL as an SFE. This classification has a ripple effect: any domestic taxpayer receiving "material assistance" from an SFE—including through licensing or technical service payments—may be disqualified from receiving clean energy tax credits.

Chairman John Moolenaar has formally questioned whether Ford’s recent efforts to repurpose the Marshall facility for energy storage and data centers constitute a modification of its original licensing agreement. This is a critical legal distinction because the OBBBA includes provisions that disqualify projects if their licensing terms are "updated, expanded, or otherwise altered" after the Act's enactment on July 4, 2025. If the pivot to energy storage is deemed a contractual modification, the project could lose its "grandfathered" status and face immediate credit denial.

The Material Assistance Cost Ratio (MACR) Challenge

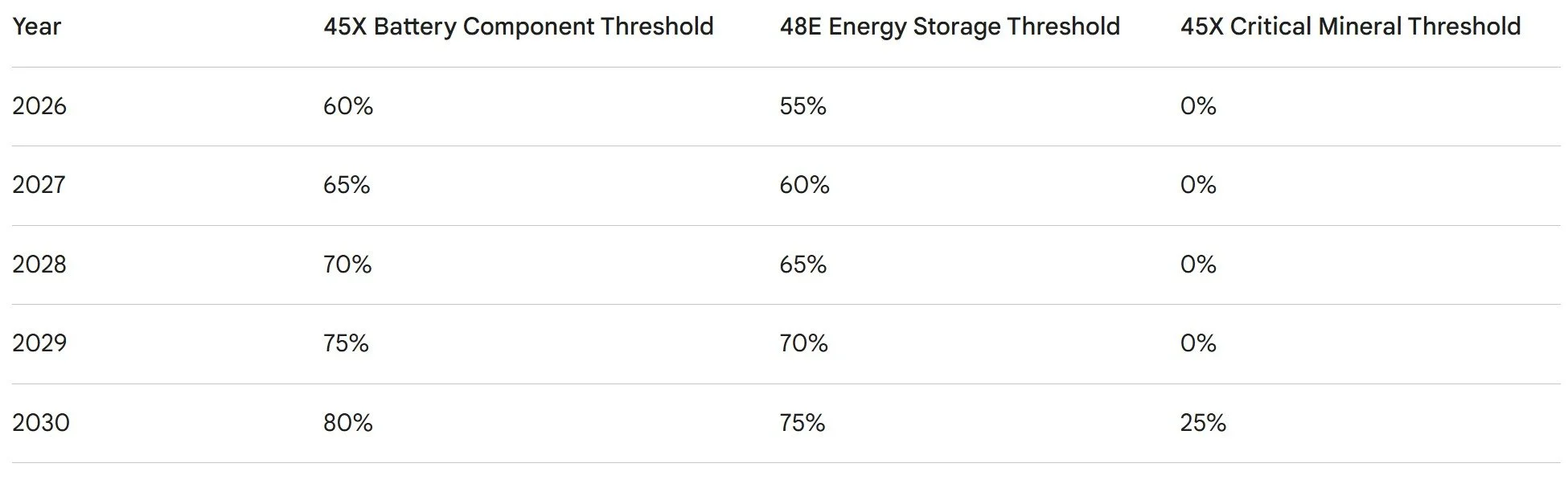

A fundamental component of the OBBBA’s anti-China strategy is the Material Assistance Cost Ratio (MACR). This ratio measures the percentage of a project’s direct costs that are derived from non-PFE sources. For a project to remain eligible for the Section 45X Advanced Manufacturing Production Credit or the Section 48E Clean Electricity Investment Credit, its MACR must meet specific annual thresholds.

For the Ford-CATL plant, which is slated to begin production in 2026, the relevant thresholds are daunting. For battery components under Section 45X, the MACR threshold starts at 60% in 2026 and escalates to 85% by 2030. For energy storage projects under Section 48E, the threshold begins at 55% and rises to 75%.

Data synthesized from.

The OBBBA provides a temporary "limited coexistence" window for critical minerals, setting the threshold at 0% until 2030. This allows Ford to use Chinese-sourced lithium, nickel, and cobalt without immediate penalty. However, the 60% threshold for "manufactured products" and components means that if the licensing fees paid to CATL, combined with the cost of any imported Chinese components (like cells or separators), exceed 40% of the project's direct costs, the plant will lose its eligibility for federal subsidies. This creates a powerful economic incentive for Ford to minimize its ongoing financial and technical dependence on CATL as quickly as possible.

Comparative Industry Strategies: Can Others Replicate the Model?

The licensing model pioneered by Ford and CATL has already begun to proliferate among other automotive manufacturers and suppliers, though with varying degrees of success and different risk profiles.

The BYD-BorgWarner Model: Tier-1 Intermediation

One of the most significant alternatives to the Ford-CATL model is the strategic agreement between BYD’s subsidiary, FinDreams Battery, and the U.S.-based Tier-1 supplier BorgWarner. Under this eight-year agreement, BorgWarner serves as the only non-OEM manufacturer with the rights to localize BYD’s "Blade" LFP battery packs for commercial vehicles in the Americas and Europe.

This structure provides a layer of intermediation between the Chinese battery giant and the American OEM. By having a U.S. supplier like BorgWarner hold the license and perform the local assembly, the OEM (such as Ford or GM) can procure a domestic battery pack without entering into a direct, high-visibility partnership with a Chinese firm. However, this model faces the same MACR risks as the Ford-CATL deal. Because BYD still supplies the underlying "blade cells" used in the packs, the value of those cells must be factored into the MACR calculation. If the cell value is too high, the final vehicle may still fail to qualify for tax credits.

The Minority Stake Model: Amplify Cell Technologies

A more traditional joint venture approach is being utilized by Amplify Cell Technologies, a partnership between Accelera by Cummins, Daimler Truck, and PACCAR, which selected Marshall County, Mississippi, for its factory. In this arrangement, the three Western partners each own 30% and jointly control the business, while EVE Energy serves as a "technology partner" with a 10% ownership stake.

This 10% stake was carefully chosen to remain well below the 25% ownership threshold that triggers FEOC or PFE status based on equity. However, analysts have noted that the 15% debt threshold under the OBBBA could be a vulnerability if EVE Energy or related Chinese banks provided significant financing for the $2-3 billion factory. Furthermore, the project had to undergo a voluntary notice to the Committee on Foreign Investment in the United States (CFIUS), highlighting the increased regulatory scrutiny on even minority Chinese participation.

The Failure of the Direct Investment Model: Gotion Michigan

The most contrasting case study is that of Gotion High-Tech’s proposed $2.4 billion battery component plant in Mecosta County, Michigan. Unlike Ford’s licensing model, the Gotion project was a direct investment by the Chinese firm’s U.S. subsidiary. Despite having Volkswagen as a 25% shareholder, Gotion faced a "barrage of protests" and legal challenges from local residents and Republican lawmakers, who cited concerns over CCP ties and national security.

The controversy culminated in late 2025 when the State of Michigan clawed back over $23 million in subsidies after local officials revoked the plant’s access to the water supply. By March 2026, the project was declared "no longer viable," with Gotion seeking damages for contract breach. The failure of the Gotion project serves as a stark warning that direct Chinese ownership of American manufacturing assets is currently politically untenable, regardless of the corporate structure or Western shareholders involved.

Technological Sovereignty vs. Dependency: The Long-Term Outlook

A central debate among industry experts is whether the Ford-CATL partnership achieves its stated goal of helping the U.S. "catch up" to China or if it simply embeds a permanent technological dependency. Ford CEO Jim Farley has argued that the best way to compete with China is to "get close to the IP" and master the manufacturing process domestically. By licensing the technology now, Ford hopes to develop its own independent, low-cost battery R&D capabilities for the next generation of vehicles.

However, there is evidence that the technology being shared by CATL is not its most advanced. Due to concerns within the Chinese government regarding technology leakage, insiders report that CATL has only transferred "older-generation" intellectual property, particularly regarding energy density and manufacturing efficiency. This suggests a "technology treadmill" where American manufacturers may remain at least one cycle behind their Chinese counterparts. Furthermore, the "effective control" rules in the OBBBA are specifically designed to prevent arrangements where a licensee remains technically dependent on the licensor for troubleshooting and upgrades.

The broader implication is that the "Ford-CATL model" of licensing may be a transitional strategy. As the OBBBA’s MACR thresholds rise toward 85% by 2030, Ford and other manufacturers will be forced to either innovate past the licensed Chinese technology or find alternative suppliers in "allied" nations like South Korea or Japan. Already, there are signs of this shift; Ford has explored potential battery arrangements with Korean firms like SK On and LG Energy Solution, though recent market slowdowns have led to the dissolution of some of these joint ventures.

Conclusion: Strategic Recommendations for Navigating the PFE Era

The Ford-CATL partnership stands as the most sophisticated attempt to date to domesticate Chinese battery technology. While it successfully bypassed the initial 25% ownership threshold of the IRA era, the OBBBA of 2025 has significantly raised the stakes. The project’s eligibility for billions in federal tax credits now rests on its ability to prove a lack of "effective control" by a PFE and to meet aggressive MACR targets for domestic value-add.

For Ford and other companies attempting to replicate this model, the following insights are paramount:

Avoid Contractual Modifications: Any updates to the licensing agreement to accommodate new markets like energy storage must be handled with extreme care to avoid losing grandfathered status under the OBBBA.

Rapid Supply Chain Localization: The "limited coexistence" on critical minerals ends in 2029. Efforts to source lithium and nickel from non-PFE entities must begin immediately to meet the 25% threshold in 2030.

Tier-1 Buffering: The BorgWarner-BYD model suggests that utilizing Tier-1 suppliers as the primary holders of Chinese licenses may reduce the political visibility and direct risk for the OEM, though it does not eliminate the MACR challenge.

Operational Independence: To avoid an "effective control" designation, manufacturers must demonstrate that they possess all the technical data and know-how required to operate and maintain their facilities without ongoing assistance from Chinese personnel.

Ultimately, the Ford-CATL partnership is an experiment in industrial policy. Its success will determine whether the United States can bridge the "battery gap" with China through strategic cooperation or if the decoupling mandated by the OBBBA will force a more painful, but perhaps more sovereign, path toward domestic energy security. The next five years will be decisive as the MACR thresholds escalate and the political scrutiny on "military-linked" partners intensifies.