Blog 5: Navigating Chinese-US BESS Manufacturing Partnerships in 2026

As the US BESS market shifts toward domestic manufacturing, Chinese integrators are finding a new path to entry: partnering with US firms to build the "rest of the box" while managing immense regulatory and financial risks.

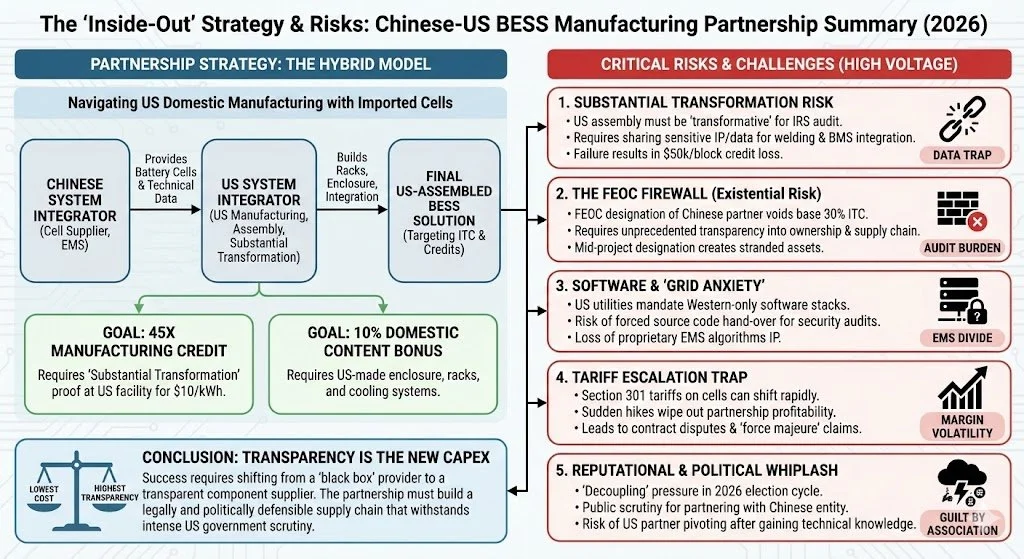

The landscape for energy storage in 2026 is defined by a paradox: the world’s most advanced battery expertise often resides in China, while the world’s most lucrative incentives for deployment are in the United States. For a Chinese BESS system integrator, the traditional "export a finished container" model is effectively dead due to 2026 tariff structures and FEOC (Foreign Entity of Concern) restrictions.

The new strategic frontier is the Hybrid Manufacturing Partnership. In this scenario, the Chinese integrator provides the high-tech heart of the system—the battery cell—while a US system integrator takes the lead on domestic manufacturing, assembly, and "Substantial Transformation" of the final BESS solution.

However, this "Inside-Out" strategy is fraught with high-voltage risks that both parties must navigate.

1. The "Substantial Transformation" Risk (45X Compliance)

Under current 2026 regulations, simply putting a Chinese cell into a US box is not enough to secure the $10/kWh Section 45X tax credit.

The Threshold: The US partner must prove "Substantial Transformation" occurred at the US facility.

The Data Trap: The Chinese partner must provide granular technical data—often considered sensitive IP—to the US partner to facilitate the automated laser welding and BMS integration required for an IRS audit trail.

The Cost of Failure: If the IRS deems the US assembly "insufficiently transformative," the $50,000 credit per 5MWh block evaporates, instantly breaking the project's financial model.

2. The 2026 "FEOC" Firewall

The most existential risk for a Chinese integrator is the FEOC designation. As of 2026, the "sticks" of the Inflation Reduction Act are fully realized.

ITC Eligibility: If the Chinese cell supplier is designated a FEOC, the entire project becomes ineligible for the base 30% Investment Tax Credit (ITC).

The Audit Burden: The US partner will require unprecedented transparency into the Chinese firm's ownership, government ties, and upstream material sourcing (lithium, cobalt, nickel).

Stranded Assets: A mid-project designation change can turn a multi-gigawatt pipeline into a stranded liability that no US tax equity investor will touch.

3. Software and "Grid Anxiety"

Energy storage is now classified as critical infrastructure. The US government is increasingly wary of software "backdoors" in grid-connected assets.

The EMS Divide: While the Chinese partner may have superior Energy Management System (EMS) algorithms, US utilities often mandate a "Western-only" software stack.

Cybersecurity Audits: The Chinese integrator may be forced to hand over source code for "black box" testing by US security agencies, risking the loss of their most valuable intellectual property.

4. The Tariff Escalation Trap

The US partner is building the enclosure, racks, and cooling systems domestically to capture the 10% Domestic Content Bonus. However, the imported cell remains the most expensive component.

Margin Volatility: Ongoing trade tensions mean Section 301 tariffs on Chinese cells can shift with little notice.

The Contract Squeeze: If a sudden 25% tariff is applied to cells, the US partner may no longer find the partnership profitable, leading to "force majeure" claims and protracted legal battles.

5. Reputational and Political Whiplash

In a 2026 election cycle environment, "decoupling" remains a potent political theme.

Guilt by Association: A US partner may face public or congressional scrutiny for partnering with a Chinese entity, even if the partnership is 100% legal.

Pivot Risk: The US partner may use the Chinese firm’s IP to bridge their technical gap, only to "pivot" to a non-Chinese cell supplier once their own supply chain matures.

Conclusion: Transparency is the New CAPEX

For a Chinese integrator, the old competitive advantage of "lowest cost" is now secondary to "highest transparency." To succeed in a partnership with a US manufacturer, Chinese firms must be prepared to act as transparent component suppliers rather than "black box" solution providers.

The partnership is no longer just about engineering; it is about building a legally and politically defensible supply chain that can survive the intense scrutiny of the US Treasury and the Department of Energy.